Why the Tories lost it

Or how opposition parties after Covid are playing politics on easy mode

Recently the Leader of the His Majesty's Most Loyal Opposition stood up in the House of Commons and slammed the Prime Minister for the mortgage crisis that occurred under his government’s watch.

“This Prime Minister is not worth the cost of mortgage payments which are already up 150%!”

No, that wasn’t Keir Starmer dunking on the Tories. It was Pierre Poilievre - the leader of the Canadian Conservative Party slamming Justin Trudeau’s Liberal Party government.

In Canada, the mortgage crisis has finally shone a light on a preexisting acute housing crisis, and channelled it into a political molotov cocktail blowing chunks out of Trudeau. The issue with housing affordability had been humming along in the background of course, but crucially the burgeoning disaster of far too few homes being built had until this point only really affected those without a significant political voice.

The pain fell upon young people, renters, and those who could not rely on family funds for help. A large and powerful political coalition on the other hand enjoyed ever increasing house prices, insulated from the pain of massive debt thanks to a near zero interest rate environment.

Many of those who made it on to the housing ladder neither felt the weight of the enormous debt they had taken on, nor did they truly internalise how over-leveraged they really were. Until rates began to rise, that is.

Suddenly, the housing crisis is being felt by the more politically powerful. Suddenly the housing crisis matters.

This phenomenon - people having borrowed hundreds upon hundreds of thousands of pounds - is why a couple of percentage points rise in interest rates hits quite so acutely, by some measures the (modest by historical standards) rates we see today are in fact felt more painfully than the far higher rates experienced in the early 90s.

Paying 15% interest on a few tens of thousands of pounds borrowed is less painful than 5%+ on hundreds of thousands of pounds borrowed.

And this is not a phenomenon unique to one country. That exchange across Ottawa’s dispatch boxes might as well have taken place in Westminster.

Let’s take a look at the painful spike in interest rates that Liz Truss caused in the UK:

Oh sorry, that was actually the Bank of Canada. What I meant to point to was THIS graph, spelling out the spike in interest rates that Liz Truss caused in the UK:

Oops, sorry that was the European Central Bank. Forgive me, take a look here at the devastating consequence of Liz Truss on UK rates:

Whoopsie daisy, that was actually the United States Federal Reserve. Here’s the carnage Liz Truss wrought on the UK:

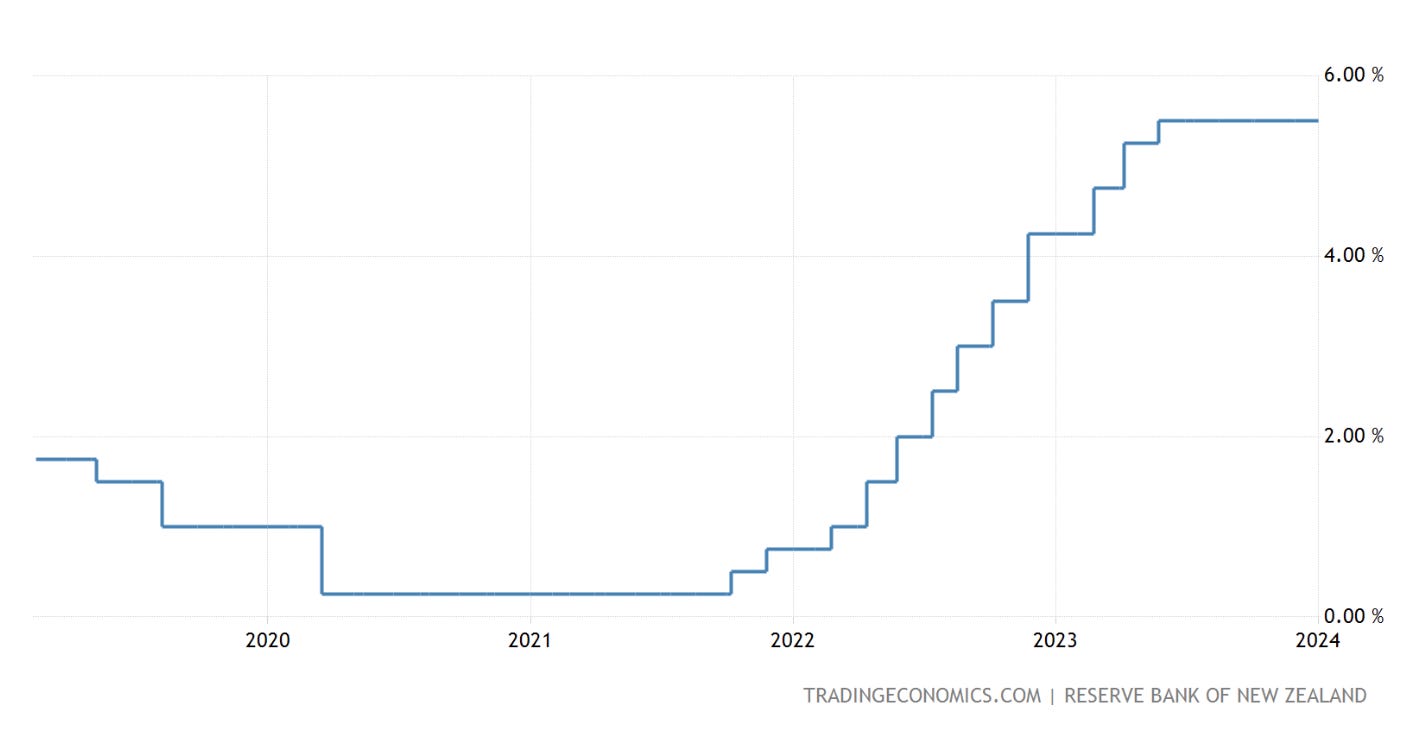

My bad, that’s New Zealand. Genuinely now, here’s the UK:

It turns out that your mortgage isn’t actually twice what it was in 2021 thanks to Liz Truss. Unless, of course, Liz Truss had power and reach that the leaders of Britain even at the height of its global empire could only dream of. Yet (sadly) last time I checked the pound sterling hasn’t made a remarkable return to global reserve currency status.

It turns out - unsurprisingly - that high interest rates are how central banks the world over respond to high inflation. Whether Liz Truss had been elected Prime Minister or not, interest rates would have followed precisely the same path. Mortgage rates, which jump around in anticipation of bank rate changes would have perhaps seen a slightly more gradual rather than jumpy ascent - but ascend they would have nonetheless. As they have the world over.

Anyone who claims their mortgage payments doubled “because of Liz Truss” is either trying to score political points or is to put it politely more than a little blinkered in their perspective of global affairs.

The point here is not that everything’s fine in the UK, quite the contrary. People are feeling the post Covid pinch, and the Labour Party have not had to work particularly hard to pin it all on the Tories.

However, this is not a story unique to Britain. As Canadian politics is highlighting - a pro planning reform opposition leader is tearing chunks out of the high inflation high mortgage rates incumbent. But this all goes far further than that.

Even in the economic juggernaut that is the United States, the Federal Reserve Bank of Kansas City has highlighted how “rising home prices and interest rates since January 2020 have more than doubled the monthly mortgage payment required to purchase a home”.

The fundamentals of how we deal with inflation (if it ain’t hurting it ain’t working) have had some fairly predictable political consequences. And it’s not looking good for incumbents in liberal democracies the world over - no matter their political complexion.

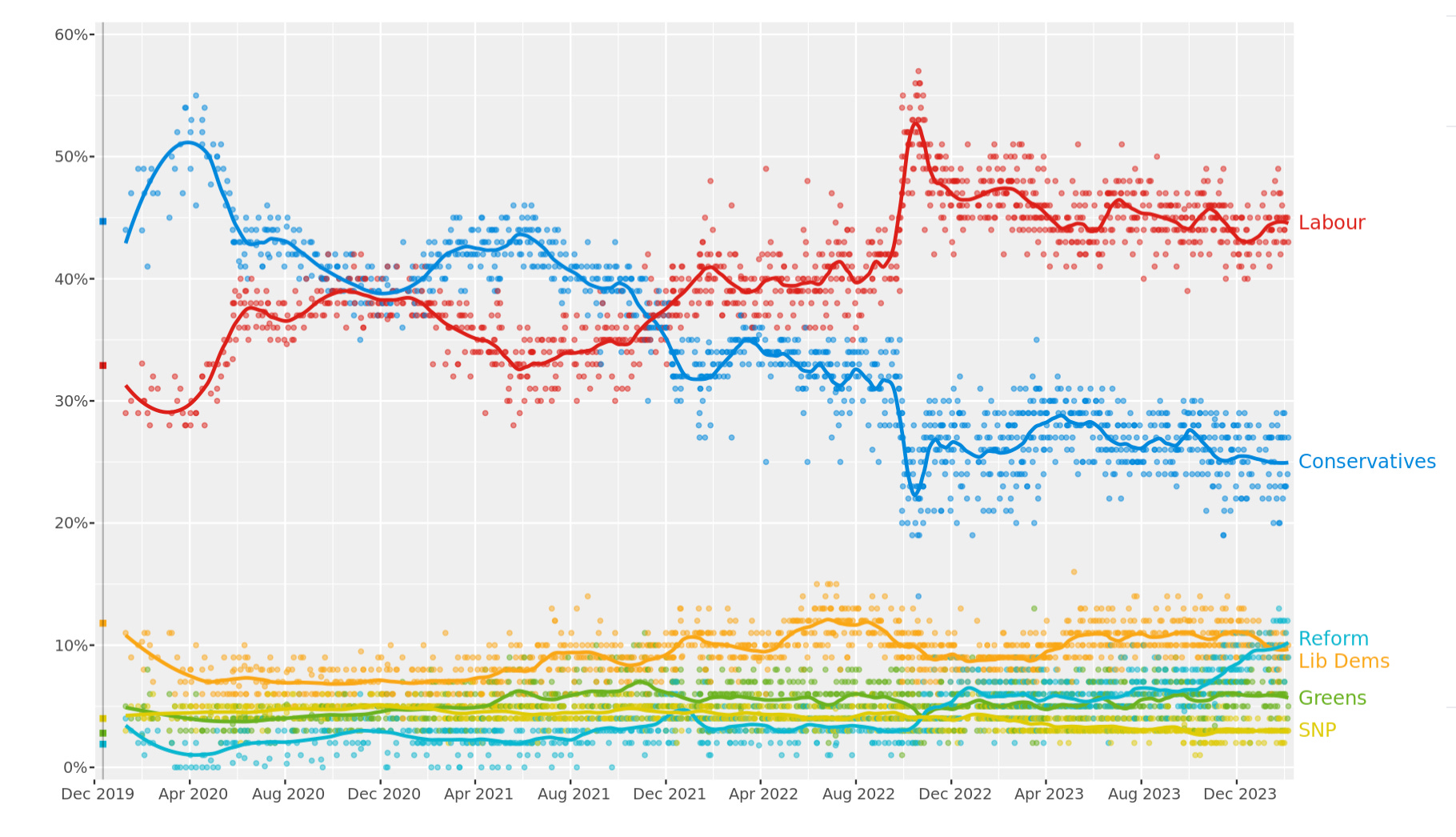

In Canada the Liberals (Red) are in government, propped up by the New Democrats (orange). Look what’s happened to the official opposition - the Conservatives (Blue). They have soared above Trudeau, in much the same way Labour has soared above the Tories here in the UK.

In the United Kingdom the effect was more sudden, but just as stark:

New Zealand had its election just a few months ago. Labour (Red), a party that had won an astonishing victory with 50.01% of the party vote at the height of the pandemic, crashed down to 26.91% just three years later. The Nationals (Blue) took power.

In Germany the SDP won a stunning victory in 2021. Today, they are battling with their coalition partners the Greens for third place. Opposition parties the CDU and AfD have seen huge rises in their support.

And even in the United States, remarkably, opposition politician Donald Trump is regularly beating incumbent Joe Biden in the polls. This despite an impressive US economic comeback and a series of serious federal indictments for Mr. Trump. The shadow of high inflation and increased interest rates is long, and strong growth takes serious time to be felt.

Against any other backdrop the American economic recovery: 2.5% growth in 2023 (compared to French growth of 0.9%, UK growth of 0.5%, and German growth of negative 0.3%) would see the incumbent enjoying a comfortable lead.

But against the backdrop of the highest inflation in decades - bedding in a permanently higher price level and combatted with early and sharp interest rate rises, even strong growth isn’t yielding the electoral dividends it might have been expected to in normal times.

As we can see the world over, in 2023/4 opposition parties are playing politics on easy mode.

Ultimately, this is politics. In the United Kingdom, the Conservatives and Liberal Democrats enjoyed playing politics on a relatively easier setting against the backdrop of the Global Financial Crisis - albeit many more journalists took the time to explain to the British public that the recession was global then than do to explain the interest rate rises are global today.

Perhaps the most poignant analysis of the politics surrounding the Global Financial Crisis came from a man who made his career off the back of it: George Osborne. Speaking about the financial crisis for the BBC documentary Blair & Brown: The New Labour Revolution in 2021, the former Chancellor said this:

“they would say it wasn’t their fault, I would say they contributed to it, but that’s irrelevant. The public, all they see is their livelihoods disappearing, their jobs disappearing, and it’s very very hard. When the economy collapses and you’re the people in charge particularly if you have been in charge for a long time, basically your time is up.”

These words, describing Labour in 2010, could just as easily be applied to the Tories today.

Postscript:

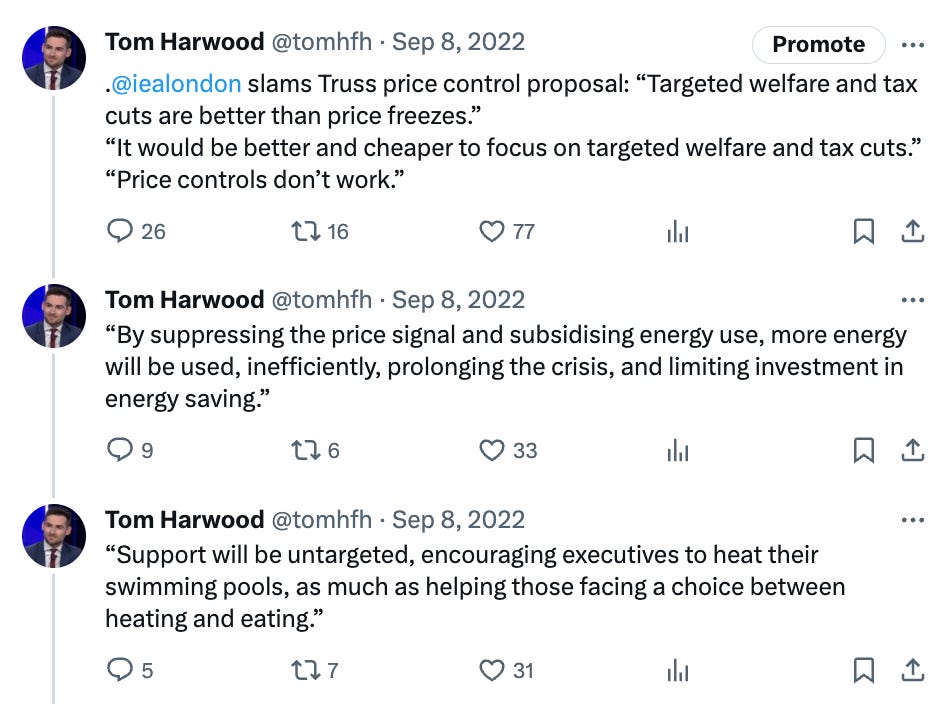

This isn’t to say that Liz Truss made no mistakes, of course. As I have written in these pages previously, the real problem with her stint in Number 10 was the extra spending she committed to, adopting Keir Starmer’s bonkers and unfunded universal plan. The socialist price control was estimated to cost £100bn-£200bn to fix the energy prices of every household, no matter poor or rich or very very rich.

As the Institute of Economic Affairs wrote at the time of the announcement, “Support will be untargeted, encouraging executives to heat their swimming pools, as much as helping those facing a choice between heating and eating.” This was the real folly.

Somehow despite this the Liz Truss episode has been painted as a lesson in going ‘too free market’. “The markets don’t like free market politicians” has become the dimwitted joke.

Is it true that markets hate free market capitalism? Why don’t we raise our horizons to observe a libertarian leader elsewhere in the world, who instead of announcing a potential £200bn in extra spending, instead announced spending reductions, cuts to red tape, and mass privatisation. Here’s how the Financial Times reported market responses to Javier Milei’s legislative agenda:

“Markets have responded positively to Milei’s plans. Argentina’s deeply distressed 2030 dollar bonds, some of the most liquid, have risen 22 per cent since November’s election to 37 cents.”

Truly, Truss simply wasn’t free market enough. Not that an absence of loss of market confidence would have changed the fundamentals. Inflation would always have soared, as it did everywhere. Rates were always going to rise, as they did everywhere. And everyone was always going to feel the pinch. As they are everywhere.

Sometimes the tide simply turns and it takes an absolute miracle for any incumbent to convince people it’s not their fault.