Persistent knobheadery

How almost two decades of policy disaster in Britain have led us to this point

It’s another week and Rachel Reeves is no happier. The government is rudderless, inflation is up, Britain confirmed its second consecutive month of negative growth, and the OBR projects that with no step change in productivity growth, debt will rise to 647% of GDP.

Growth is going backwards, inflation upwards, demographic crisis looms, and the government can’t cut a penny off public spending. The country nominally elected a moderate, prudent Sir Keir Starmer, but now his spend happy backbenchers are calling the shots.

Today the Prime Minister has sacked four MPs for rebelling on welfare cuts. Or as one Labour source put it to The Times, “persistent knobheadery”. It is unclear if these four whip removals will have the desired effect on the 100+ Labour MPs who were willing and able to overturn key fiscal policies.

And while the Prime Minister scrambles for a semblance of control, the country drifts.

It is hard to put into words just how dire a prospectus this is for what used to be the richest most dynamic economy in the world. I have written in this newsletter before about Argentina’s fall from first world to third. Could Britain be on its own Peronist path of decline?

Charting the course of how bleak things have become is painful for any vaguely patriotic person. But it is a vital exercise if Britain is to arrest its own decline.

In the beginning…

In 2008, the BBC ran an article with the headline “Britons 'richer than Americans'” - citing analysis by Oxford Economics revealing GDP per capita that year was to be £250 higher this side of the pond. Fast forward to today, and the average Brit is 40% poorer than the average American. If the UK were a US state it would now be poorer than the poorest state in the Union, Mississippi.

Last week I wrote about a number of storms that have rocked the British economy since the Global Financial Crisis. The effect of planning restrictions biting London more than ever before as its population rebounded to pre-war levels. Employment practice restrictions preventing the labour market reallocation that took place in countries like the United States. And the indulgence of nimbyism that ballooned infrastructure costs just at the moment that the state rolled back on public investment.

Well meaning early reforms of the Coalition government attempting to manage nimbyism instead supercharged it. The 2011 Localism Act introduced a requirement for those seeking planning permission to carry out a pre-application consultation, as a means to get communities on board with new developments.

The wildly optimistic idea behind this extra consultation was that earlier community dialogue would reduce later objections. It did not. Appeals and judicial reviews are at historic highs. Approvals have slowed down. It turns out that more mandatory opportunity for communities to organise and object just means more organised objection.

And it’s important to understand what the effect of this objection is. Britain saw itself as a rich country in 2008. But rich countries don’t remain rich by standing still. Britain hasn’t built a reservoir since 1992, a nuclear power station since 1995, or a new motorway since 2003. Today we see water rationing, energy rationing, and more time lost to commuting than our European counterparts. This is not a coincidence.

The longer you go without new infrastructure, the more the lack of new infrastructure bites. While we haven’t allowed the construction of a single new reservoir for a third of a century (despite water companies repeatedly and expensively applying for permission), over the same timespan our population has grown by more than 10 million.

But nimbyism is not the only disease explaining relative decline in the post-2008 world. Other countries, particularly in the Anglosphere, suffer from slow and expensive building problems too - though nowhere near to the extent that Britain has.

Again, remember that while the United States returned to its pre-2008 real GDP per capita growth trend after the crisis, the UK stubbornly has not.

Follow the money…

The economist Tyler Goodspeed persuasively hypothesises that UK capital markets have become particularly - almost uniquely - constrained in the post-2008 world.

The Global Financial Crisis ushered in a wave of global banking regulation restricting bank lending that was deemed too risky. Goodspeed argues this hasn’t particularly hurt the United States, where businesses source just 20% of external financing from banks.

UK businesses on the other hand derive 80% of external financing from big banks.

When post-crisis global banking regulation (like Basel III tier capital requirements) came along, these hampered businesses’ access to capital in the UK far more than it did in the US. This was thanks to Americans having a longstanding and diverse pool of non-bank sources of borrowing; venture capital, private equity, and angel investors, which all avoided the global banking regulation that hamstrung big UK and US lenders.

What’s more, America’s many midsize banks avoided the threshold for the most stringent global regulation. In Britain on the other hand, we have a far smaller number of very large financial institutions. The mid size banking market that helped incubate American businesses just doesn’t exist in the same way in the UK.

British businesses relied on a small number of very big banks. The very banks most hampered by post-2008 regulation. And consequently least able or willing to take risks on new ventures with high growth potential.

And that’s before you even consider how the UK instituted a bank levy in 2011, taxing banks’ liabilities and increasing the cost of capital, and the EU banned bankers’ bonuses. None of this happened in the United States.

But there is another absolutely fundamental piece of the puzzle.

It’s the energy, stupid…

Before ‘Net Zero’ there was ‘Net 80% Reduction’. Back in 2008, then Energy Secretary Ed Miliband’s Climate Change Act required the UK to reduce its greenhouse gas emissions by at least 80% by 2050 relative to 1990 levels. The Act received overwhelming support in Parliament. Just five out of 646 MPs voted against it.

Their names were Christopher Chope, Philip Davies, Peter Lilley, Andrew Tyrie, and Ann Widdecombe.

In 2019, the Act was amended, uplifting the net reduction target from at least 80% to 100% by 2050. And thus was born Net Zero.

Britain was the first country in the world to commit to legally binding long term climate change targets overseen by an independent committee back in 2008. And eleven years later Britain became the first country in the world to ramp those targets up to net zero emissions by the mid point of this century.

The 2008 Act introduced the world’s first system of Carbon Budgeting; five-year carbon budgets capping the emissions the UK can emit each half decade, progressively lowering the cap over time. These carbon budgets have been used by campaigners to block road building, oil and gas licensing, and airport expansion. They have added costs to industries like steel, cement, and chemicals - which can’t grow without expensive carbon mitigation.

Global firsts, that coincided with national stagnation.

Net Zero didn’t spring from the ether. By the time MPs nodded through the 2019 amendment, the 2008 law being amended had already got Britain half of the way to the net zero goal. Emissions were near 50% lower than they were in 1990. In this context, it’s easy to see how little debate there was around Theresa May making the push from 80% to 100% her final act as Prime Minister.

But there should have been.

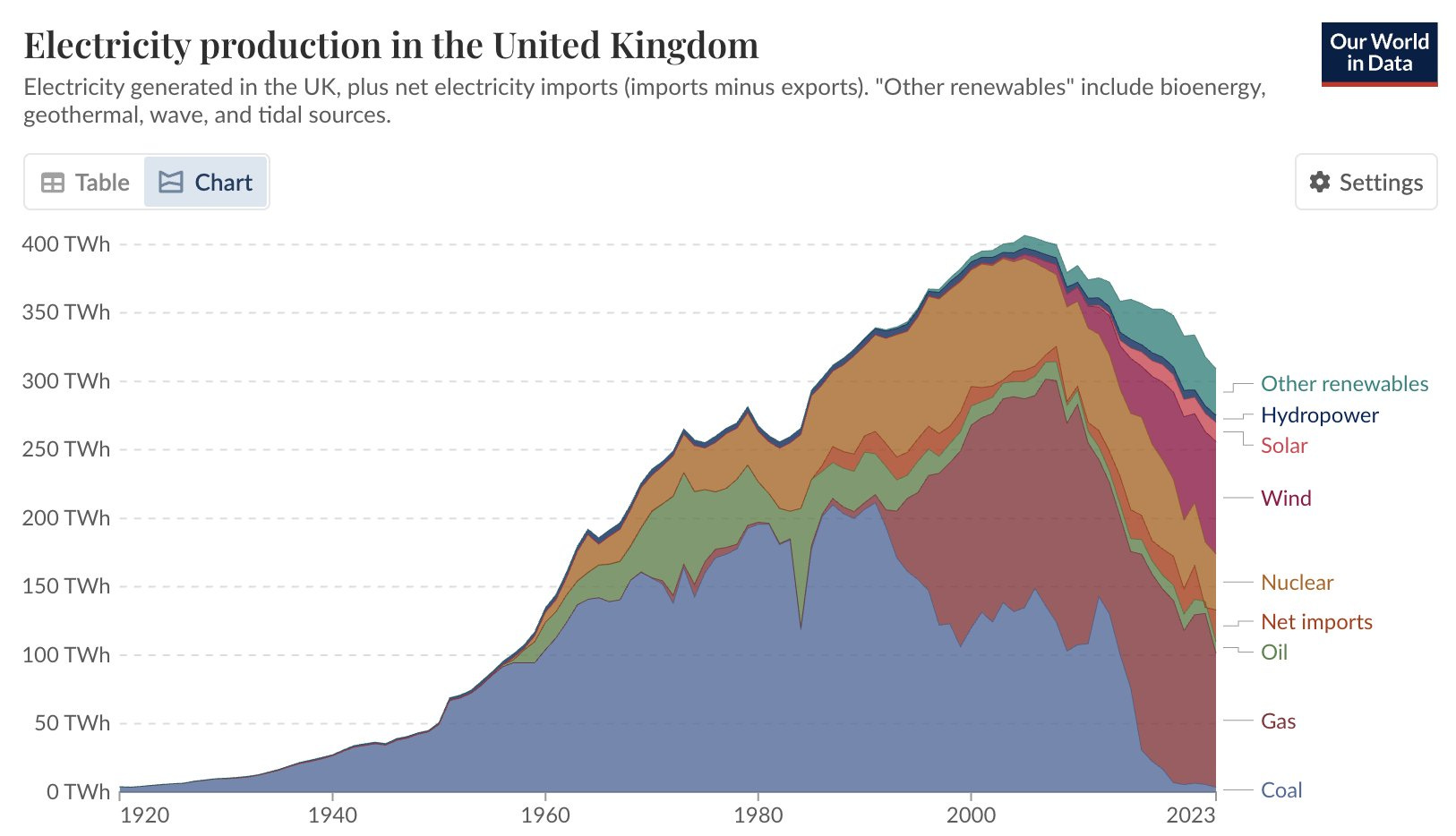

The UK has spent the years since the passage of the 2008 Climate Change Act diving headfirst into a state of relative energy poverty. Bound by legal targets and Soviet-style five year plans, the country did not wait for clean generation to be built before shutting down fossil fuel energy sources.

We drove off the energy cliff without enough clean generation in place to break our fall. Like Gromit the Dog in The Wrong Trousers, we ran out of track and simply hoped to frantically lay down more. But it wasn’t enough.

British electricity generation has fallen precipitously since the introduction of the Climate Change Act. Between 2008 and 2023, production crashed by a quarter. Down from 400 terawatt hours to just 309. In the same timeframe that electricity production fell by 25%, our population grew by 7.9 million, or 13%.

While our electricity production has fallen by 25% since 2008, the United States has expanded its electricity production by 7%. America is now a net energy exporter. And Britain has taken the opposite path.

When I was born, Britain was a net energy exporter. Electricity prices were falling, not rising. Measured by gross value added, Britain in the 1990s was the fourth biggest manufacturing economy in the world.

A Jobs Foundation report published this weekend found that from 1993 to 1998, British manufacturing employment increased from 4.1 million to 4.3 million. During this time, electricity prices dropped by a remarkable 22%.

By comparison, today Britain has fallen out of the top 10 largest manufacturing economies. The report sets out how “energy-intensive industries, including steel, chemicals, cement, paper and glass, have seen the most significant casualties. Between 2021 and 2024, chemical output declined by 40%.”

Energy is prosperity. Without cheap abundant energy Britain’s manufacturing has suffered immensely. Energy costing twice what it does in the United States has not only crippled manufacturing, it has plunged Britain into debt and taxes.

Let us not forget that far larger than any tax cut Liz Truss promised, was her ludicrous scheme (lifted from the Labour Party) to pay for half of the nation’s energy bills. Three times larger. It is worth considering whether, in a world where Britain avoids splurging more than £100bn on energy price fixing, the confidence crisis could have been avoided. Had Britain remained a net energy exporter rather than importer, 2022 could have been a very different year.

Expensive energy is an opportunity cost. Spending less on essentials like energy means less debt to accumulate, or more money to spend elsewhere. It means more economic activity, and less stagnation.

Ergophobia

Some people attempt to make the ludicrous argument that less energy production is actually a good thing. Environmentally conscious consumers and energy efficient technologies like LED light bulbs have, so goes the argument, meant we can use less energy.

But this hasn’t been the case in the United States, despite widespread adoption of technologies like LED lights. Why? Because throughout history when offered the choice between growth or stagnation, we have almost always picked the path of more, not less.

John Maynard Keynes once predicted that his grandchildren (people my parents’ age) would work just 15 hours a week. Given productivity gains, he hypothesised, why would people not work less for the same amount of money. Why not work Monday and Tuesday, and enjoy a five day weekend?

The reason why not, of course, is that banking productivity gains as holiday rather than extra production would have left us all dirt poor by today’s standards. As we become more productive, and technology becomes more efficient, we want more for ourselves and our children, not stagnation.

Foreign holidays have become cheaper over the last half century. Do we go to the same places at the same frequency and save the cash that made up the difference? Of course not. We go to fancier places, more often. Efficiency gains generally lead us to consume more, not less.

Efficiency gains should lead to better lives, not the same lives with those gains eaten up by more expensive electricity. In a world where Britain was once again an energy exporter, air conditioning - for example - would be commonplace.

In the book Where Is My Flying Car?, J. Storrs Hall coins the term ergophobia to describe fear of energy consumption. He argues that even America has stalled in its energy consumption growth since the 1970s, and imagines the technological marvels that could be achieved had the country remained on the exponential path of consuming more energy.

Between 1850 and 1970 transport technology roared from trains to steamboats, to cars to aeroplanes, to jet engines to rocket ships, to moon landings, supersonic flight, bullet trains…. and then stopped. The way we get about today looks roughly the same today as it did 50 years ago. Had energy consumption continued to rise, technological progression in how we get about could have continued on that upwards curve too.

But I digress. While America has barely grown its energy consumption per person, Britain’s has actively gone backwards. And most concerning of all we have had a generation of politicians who have revelled in this decline.

To a majority of MPs today, using less energy is seen as a good thing - not a bad thing. Blocking new projects and effectively banning creature comforts has been the raison d'etre for too many of our lawmakers. And it has made us all poorer.

The most baffling thing about this all is there is a green path to energy abundance. Stagnation is a choice. There is so much energy devoted to passing motions demanding limited emissions, but almost no energy at all going into deregulating the technologies necessary to get us there.

Small modular nuclear reactors power every Trident submarine. But years after the government expressed interest in civil applications, not a single one is yet being built. And bizarre new regulations on traditional nuclear reactors have forced the construction of Hinkley Point C to use 25% more concrete and 35% more steel than reactors in other developed countries.

We are currently building the most expensive nuclear power stations ever constructed, and their addition to the energy mix will only replace the nuclear power stations that are being switched off as they come to the end of their lives.

Some climate emergency.

Postscript

Many journalists like to pretend that 2016 was the year that things went wrong for Britain. But that’s not remotely what the data shows us. Britain, and much of Europe, has had a torrid time of things not for the past nine years, but instead the last seventeen.

The year 2008 is the crucial turning point.

Until we understand the fundamental regulatory changes that hit the United Kingdom in that year; from finance to energy to London’s green belt, we will find ourselves fundamentally unable to exit the doom loop of persistent knobheadery.